In today’s changing financial landscape, credit unions face a host of challenges when it comes to maintaining stability and ensuring member protection.

Recently, the National Credit Union Administration (NCUA) outlined its supervisory priorities for 2024, highlighting several key areas of focus.

Below we’ll breakdown what’s top of mind for credit union leaders navigating risk.

Credit Risk and Economic Environment:

Credit risk management is essential for credit unions to safeguard their financial health. Inflation and high interest rates have made credit risk assessments even more important this year. Metrics such as delinquency ratios and loan loss forecasting methods play a crucial role in identifying potential risks and implementing appropriate risk-mitigation strategies.

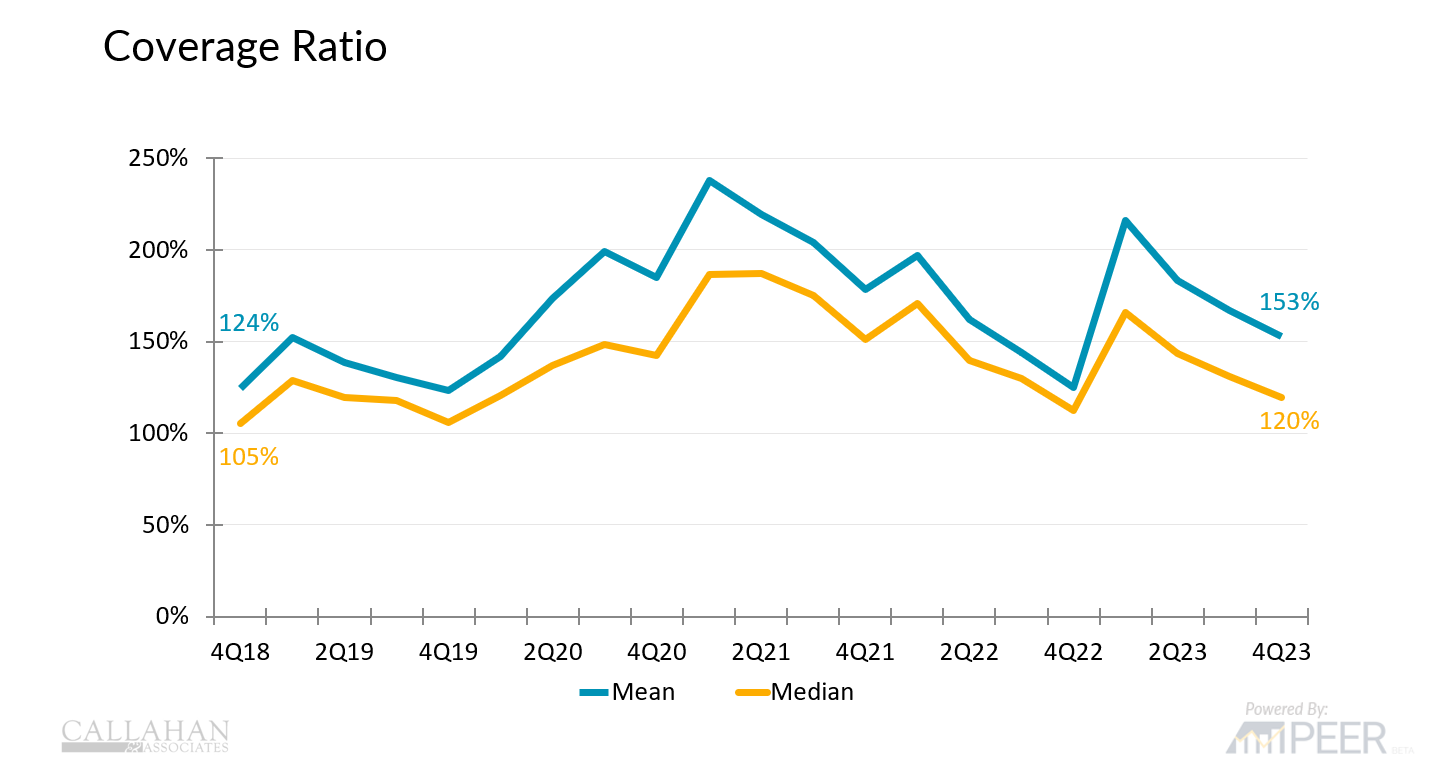

U.S. Credit Unions | Data as of 12.31.2023

-

The coverage ratio measures the amount credit unions have set aside in their allowance account relative to delinquent loans outstanding, making it an important measure of protection against credit risk.

-

As of year-end, U.S. credit unions had an average of $1.53 set aside for every dollar of delinquent loans on their books. This is still at a healthy level, but coverage declined throughout 2023 despite credit unions increasing their provision expenses.

Pro Tip For Peer Suite Users

As you prepare for upcoming regulatory conversations, we recommend leveraging the brand new 2024 NCUA Supervisory Priorities dashboard in Peer Suite.

Not yet a Callahan client? If you’re interested in viewing your credit union’s performance dashboard, complete this form and our team will be with you shortly.

Liquidity Challenges and Opportunities:

Liquidity management is paramount for credit unions to ensure their ability to meet member needs and obligations. Amid declining share growth, credit unions face liquidity challenges that require careful navigation.

Strategies for attracting deposits and leveraging liquidity to support members not only safegaurd financial stability but also enhance member satisfaction and trust.

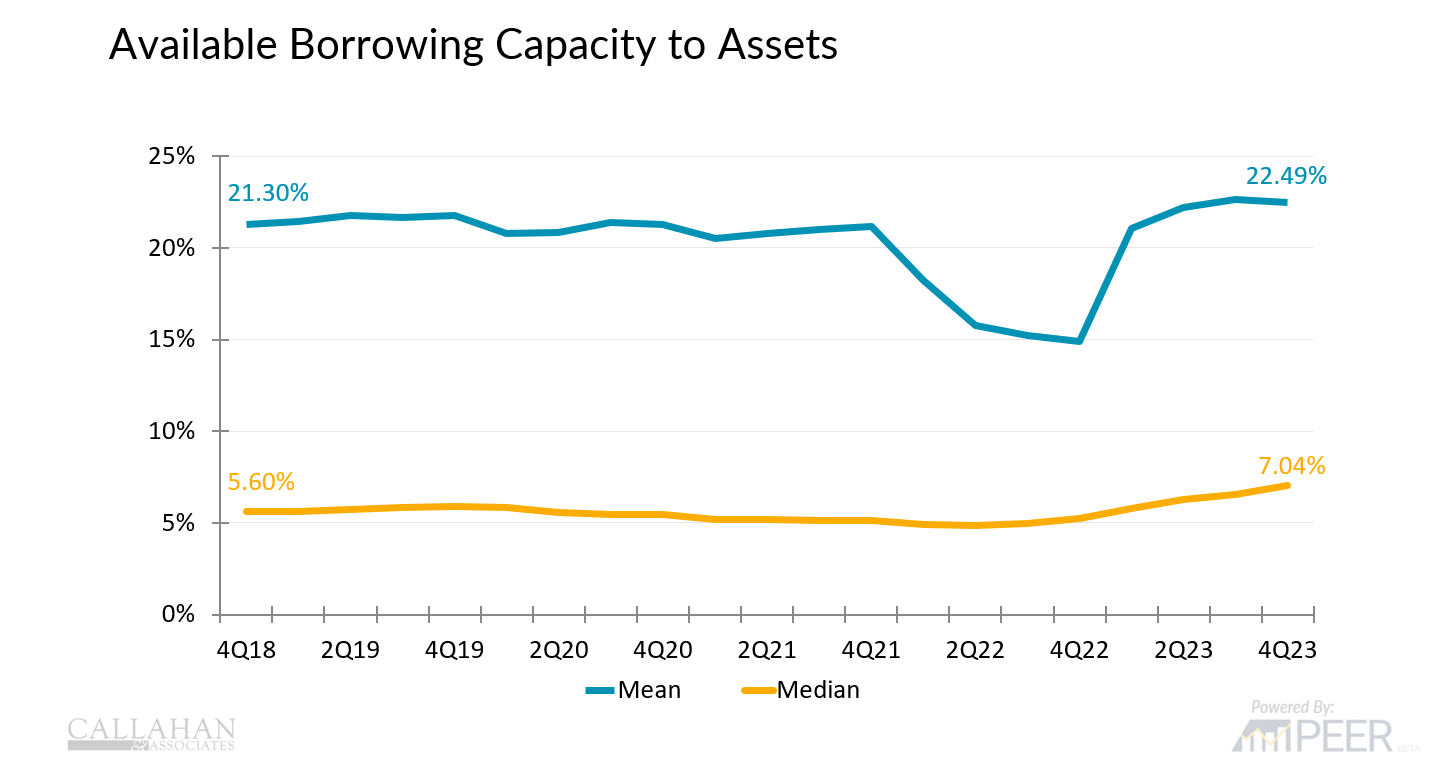

U.S. Credit Unions | Data as of 12.31.2023

-

Available borrowing capacity relative to assets measures the strength of credit unions’ liquidity safety net. This is important if the credit union needs to quickly source funds to maintain liquidity and institutional stability should economic conditions worsen.

-

The credit union industry had an available borrowing capacity of 22.49% of assets as of December 2023. This signals that the industry as a whole is prepared for potential liquidity emergencies.

Interest Rate Risk Management:

Effective management of interest rate risk is crucial for credit unions to protect their balance sheets and maintain profitability. In a volatile interest rate environment, credit unions must carefully monitor investment portfolio strategies and asset repricing practices.

Understanding the implications of interest rate fluctuations on loan paydown rates and asset valuations allows credit unions to make informed decisions and mitigate potential risks.

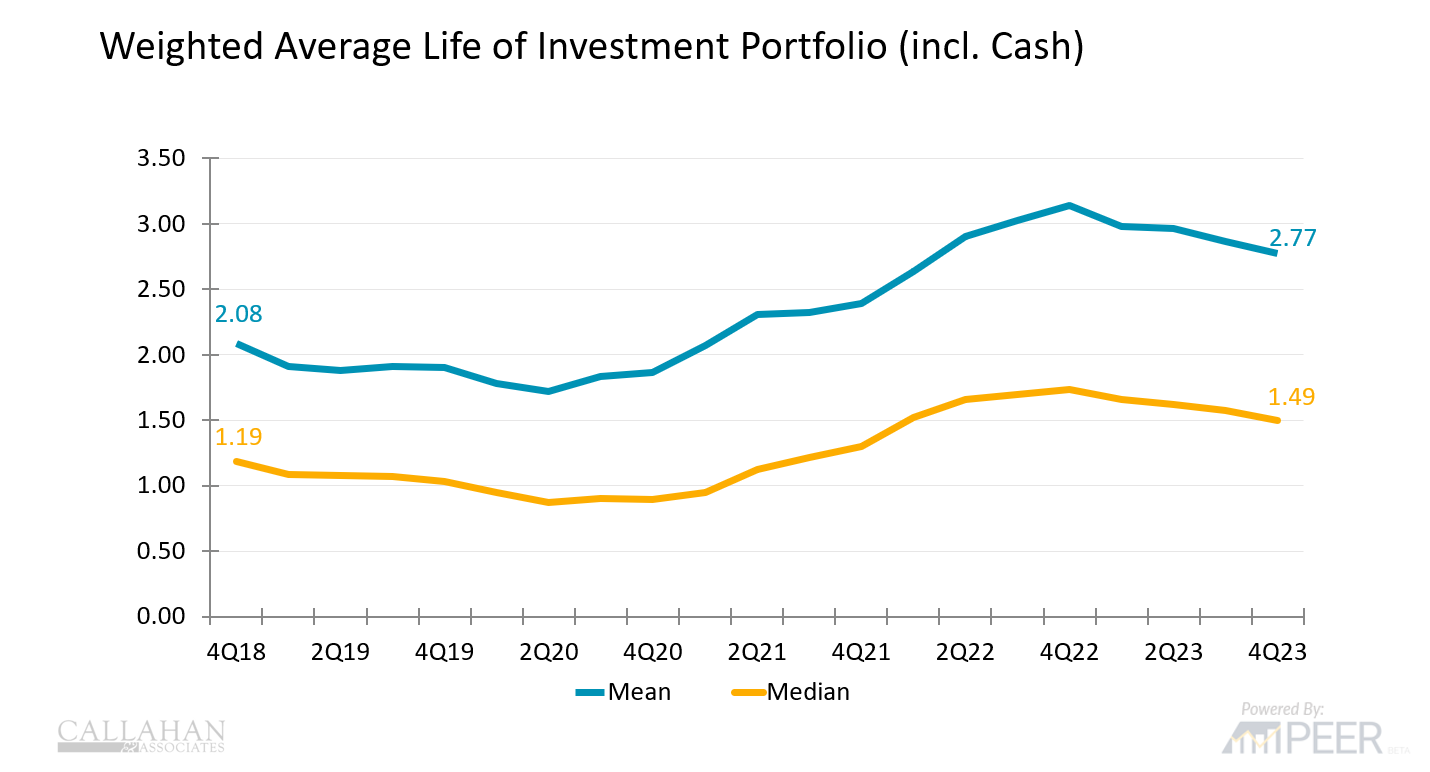

U.S. Credit Unions | Data as of 12.31.2023

-

Credit unions’ investment portfolios that hold long-term securities will generally experience more volatility when interest rates change. Credit union examiners will be watching for this.

-

The weighted average life of the industry’s investment portfolio was 2.77 years as of year-end. This is an improvement from December 2022 because credit unions slowed purchases of longer-term securities. As securities matured, credit unions kept the proceeds in cash or short-term investments to improve liquidity.

The NCUA’s 2024 supervisory priorities offer valuable guidance for credit unions. By prioritizing credit risk, liquidity, consumer financial protection, and interest rate risk management, credit unions can enhance their resilience and ensure their long-term success.

Evaluate Your Risk | Free Performance Dashboard

With a focus on liquidity, credit, and interest rate risk focus areas, we’ll help you uncover your institution’s performance against local and industry-wide peers.

We request 30 minutes of your time to create a peer group that’s most relevant to your institution, and you’ll get to keep the results for free.

More Blogs

Greater Texas Integrates AI In HR Without Losing The Human Touch

A real-world look at how a $980 million credit union applies AI in HR to reduce busy work, improve hiring, and protect human decision-making.

How To Put Financial Wellbeing Strategy Into Practice

Patelco Credit Union shows how it translates a clearly defined financial wellbeing strategy into everyday practices to drive measurable improvements in the member experience.

4 Ways To Build A Meaningful Employee Recognition Program

In a Callahan client webinar, Rob Hoyle explains how Vantage West keeps credit union employee recognition meaningful, merit-based, and materially rewarding.

The Risk Of FOMO In Credit Union Leadership

Fear of missing out can drive credit union leaders to make big decisions for the wrong reasons. Recognize it, and learn to lead with clarity, purpose, and intentionality instead.

Callahan & Associates And Quantum Governance, L3C™ Unite to Advance Credit Union Governance

Callahan & Associates, a leading provider in performance measurement, leadership development, strategic advisory, and community development for credit unions, is excited to announce the acquisition of Quantum Governance, a nationally recognized consulting firm specializing in governance and strategy.

Tips To Make A Core Conversion Easier

Best practices for credit union core conversions.

Accessible Financial Services Matter More Than Ever

For millions of Americans, accessible financial services remain out of reach. In St. Louis, MO, Alltru FCU is changing that.

How To Use Credit Union Marketing Personas To Deepen Relationships

Rich knowledge of member behavior helps Solarity Credit Union segment its membership, create useful credit union marketing personas, and focus on deepening engagement.

How To Benchmark Credit Union Performance Against The Economy

Credit union executives and finance leaders face an increasingly complex task: explaining financial performance in a way that is both accurate and actionable. Traditional benchmarking approaches focus on two perspectives: Internal Trends – How your own institution’s...

Why Who You Benchmark Performance Against Matters More Than You Think

Too often, benchmarking is treated as a scorecard — a way to check performance against peers for board prep, audits, or strategic planning discussions. But the choice of peer group matters, it can help you tell a more complete story about your credit union’s performance and validate strategic decisions.